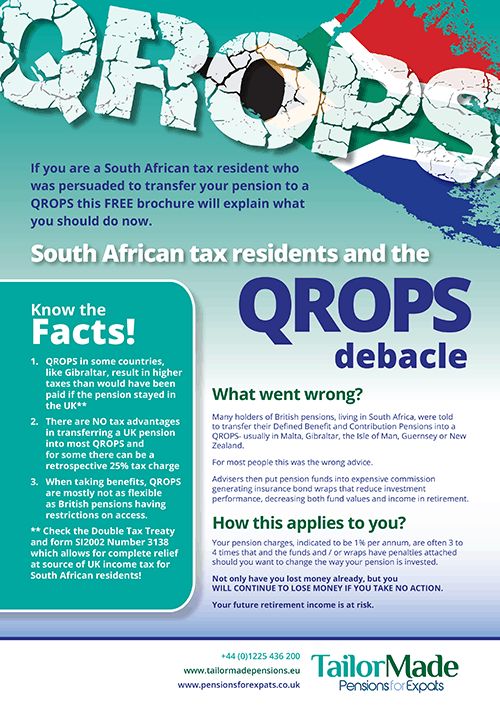

QROPS debacle hits expatriates where it hurts – retirement

Be aware of the QROPS debacle that has affected thousands and keep your pension safe. Many Spanish expats will be offered offshore insurance bonds for their investments and pensions, and now they are paying the penalty.

No tax advantage by moving your pension offshore

Offshore advisers are constantly promoting QROPS without making reference to the UK and Spain Double Tax Treaty – don’t get caught out!

South Africa

If you live in South Africa, have a UK pension, QROPS or have been advised to take out an Investment Bond or wish to receive high quality investment advice taking into account Double Tax Treaties, then we are able to assist you.

For many expats living in South Africa the key issues or concerns are summarised by us, with some pointers as to how you can avoid the mistakes that we commonly see, and consider the things that make a difference to every South African expat.

We regularly blog on the latest matters affecting you, and within these pages we have put together South African specific pension information for expats. We also focus on the main tax considerations for expats in South Africa and then go onto to discuss specific investment strategies including the pro’s and cons of investment bonds.

Background

There were 300,000 UK-born people with residency in South Africa in 2016, according to the South African statistics agency, which used figures reported by South African authorities. Of these, very few receive the UK state pension.

For expats that need advice on pensions and investments, the investment regulator is here www.fsb.co.za.

For those that need advice on insurance, whether that be car insurance, health insurance or life insurance, the insurance regulator is here www.fsb.co.za.

Aisa Group is registered for both insurance and investment advice for expats resident in South Africa.

South Africa Specific Pension Information

All pensions originating from the UK are subject to tax in South African unless they are pensions being paid in respect of service to the government (e.g. civil service) or local government (but not teaching). These exceptions are taxed in the UK instead.

![]() KEY POINT: Pensions - UK pensions can be paid without deduction of UK tax if you are resident in South African and don't spend too many days a year in the UK.

KEY POINT: Pensions - UK pensions can be paid without deduction of UK tax if you are resident in South African and don't spend too many days a year in the UK.

If you go to the UK Revenue and Customs site www.hmrc.gov.uk, you will be able to find both an English language version of the current UK-South African Double Taxation Treaty www.gov.uk (articles 18 and 19 refer to pensions).

You can find a down-loadable DT-Individual form enabling you to claim exemption from UK tax (i.e. be tax-coded "NT") and to obtain a refund of UK tax already paid (within the last 4 tax years). You will have to get the form certified by the South African tax authorities.

![]() KEY POINT: Trusts governed by foreign law are generally analysed by applying conflict of law rules. As a result, in South African, trusts can be subject to both income tax and gratuitous transfer taxes. Some pensions are not regarded as Trusts!

KEY POINT: Trusts governed by foreign law are generally analysed by applying conflict of law rules. As a result, in South African, trusts can be subject to both income tax and gratuitous transfer taxes. Some pensions are not regarded as Trusts!

South Africa Tax considerations

South African only recognises investments, investment providers and insurance bonds that are registered to be sold in South Africa. There is a suggestion that the sale of non-compliant insurance bonds (whether outside a pension or not) will not enjoy any tax benefits and should be declared on tax returns, but certainly non-regulated investments do not come under any form of protection.

![]() KEY POINT: Trusts governed by foreign law are generally analysed by applying conflict of law rules. As a result, in South African, trusts can be subject to both income tax and gratuitous transfer taxes.

KEY POINT: Trusts governed by foreign law are generally analysed by applying conflict of law rules. As a result, in South African, trusts can be subject to both income tax and gratuitous transfer taxes.

The legal and tax consequences of a foreign trust are complex and uncertain. Case law is scarce. For an expat living in South African, or returning to the UK they have to consider personalised bond rules to avoid taxation in the UK, and they have to consider trust implications and income tax in South African.

![]() KEY POINT: For those expats who were advised to take out a trust in the UK and put the investment into an Investment Bond for tax efficiency reasons – you must review this arrangement through a combined UK and South African wealth adviser who has Inheritance Tax specialities (such as ourselves), especially if the expat intends to return to the UK.

KEY POINT: For those expats who were advised to take out a trust in the UK and put the investment into an Investment Bond for tax efficiency reasons – you must review this arrangement through a combined UK and South African wealth adviser who has Inheritance Tax specialities (such as ourselves), especially if the expat intends to return to the UK.

South Africa specific Investment Strategies

Offshore Investment bonds, or Offshore Insurance Bonds (known as wrappers) that are sold on a commission basis should not be used for investments, nor pensions that are transferred. Commission based bonds are often opaque and expensive, with hefty exit fees in the early years. The fact is that where an Offshore Investment bonds, or Offshore Insurance Bonds is appropriate it can be obtained from the same providers without commission and far reduced annual cost, thus reducing the risk required to obtain the same returns.

![]() KEY POINT: If the fees for a tax strategy are higher than the tax saved, then it would be sensible to look at taxed options with lower fees. When we review existing products often recommended in South African, we discover many cases that the clients would have been better off not taking out the supposedly “tax-efficient” investment bond!

KEY POINT: If the fees for a tax strategy are higher than the tax saved, then it would be sensible to look at taxed options with lower fees. When we review existing products often recommended in South African, we discover many cases that the clients would have been better off not taking out the supposedly “tax-efficient” investment bond!

The adviser should look at alternative strategies, suggest options to discuss with you, finalising a best solution for you, the client, based on investment, fees and the overall tax liability. There is a suggestion that the sale of non-compliant insurance bonds (whether outside a pension or not) will not enjoy any tax benefits and should be declared on tax returns, but certainly non-regulated investments do not come under any form of protection.

![]() KEY POINT: Investments not regulated under South African rules will not be considered or protected by any local regulators. If these investments go bust then the client will lose all their money and have no protection.

KEY POINT: Investments not regulated under South African rules will not be considered or protected by any local regulators. If these investments go bust then the client will lose all their money and have no protection.

Key issues / concerns

Investments not regulated under South African rules will not be considered or protected by any local regulators. If these investments go bust then the client will lose all their money and have no protection.

Investment bonds, when sold in a QROPS or International SIPP, are to be avoided. Some investment bonds can be helpful but only with regulated investments inside and a “clean” structure (no commissions).

The main consideration should be the balancing of tax efficient advice which takes into account future plans, and charges of products.

If the fees for a tax strategy are higher than the tax saved, then it would be sensible to look at taxed options with lower fees. When we review existing products often recommended in South African, we discover in many cases that the clients would have been better off not taking out the supposedly “tax-efficient” investment bond!

The vast majority of expat advisers (differ from regulated South African advisers), providing investment or pension investment advice to UK expats, do not have investment licences and are circumventing this by selling insurance wrappers that are expensive and commission laden.

What should you be considering?

1. If you are confident enough, then do your research, and place investment directly.

2. If you need assistance, then seek advisers who are regulated themselves in the UK for pensions advice, and / or regulated for INVESTMENT advice in South Africa.

3. Consider not only tax efficiency, but also costs!

4. Point 4 – is, make sure the costs are accurate! If you are told the costs are 1% or 1.5% per annum in total and there is no fee up front, then you are probably being lied to in 95% of cases.

Some advisers, providing investment or pension investment advice, do not have investment licences and are circumventing this by selling insurance wrappers (investment bonds) that are expensive and commission laden.

Don’t get taken in by the great claims over QROPS and Insurance bonds or investment platforms that are really investment bonds. These add layered charges and are usually not the best outcome for clients (although we accept that in around 15% of cases they are).

Don’t be a sheep. Just because your best friend was advised to do something, never assume this is the right thing. Each person is an individual and requires individual solutions. If your friend were to walk off a cliff, would you follow them?

Our Empirical evidence from clients we have spoken has shown us that many expat sales advisers in South Africa, just sell a product to their clients for commission and do not provided financial solutions. The product is often a QROPS or an International SIPP or an investment bond, which may or may not be the best advice but this is not really considered. Don’t listen as 85% of the time you would be better off doing something else with your hard earned money or pension.

Regulatory Statement

Pensions for Expats is registered with the FSB as Aisa International (PTY) Ltd – No. 47638 and authorised for provision of intermediary services.

Trading Names: Pensions for Expats is a registered trading name, but does not provide expat pension advice in that name. This website is aimed at individuals not resident in the UK. Please see www.aisagroup.org in order to ensure that you are dealing with the most appropriate group company.